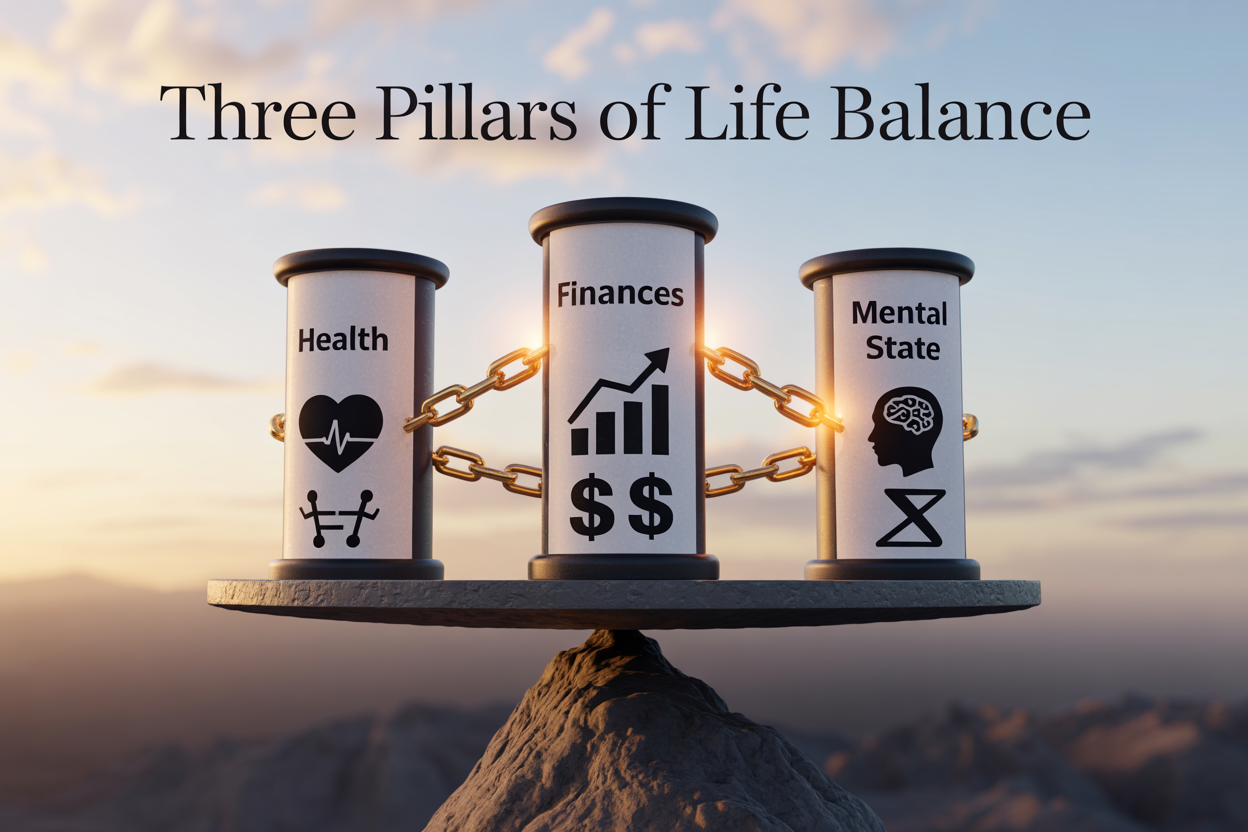

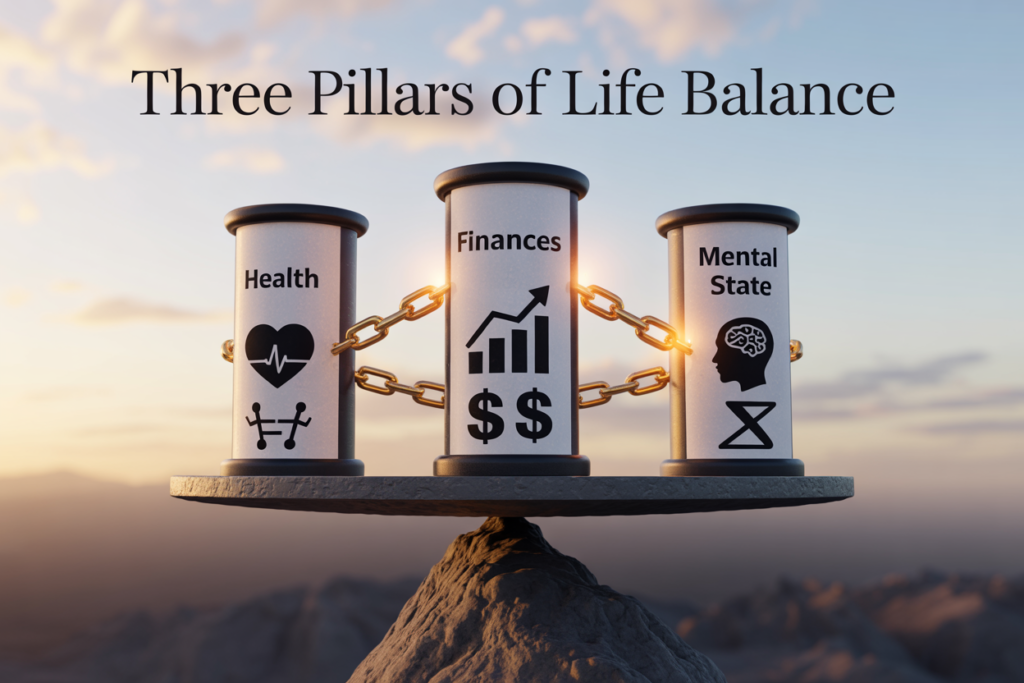

Life balance is being able to juggle everything perfectly no; it’s about the understanding how health, money, and mental state work with one another in a machinery of gears.

This guide is for busy professionals, parents, and anyone who feels like they’re winning in one area of life while everything else falls apart. You know the feeling: you’re crushing it at work but your health suffers, or you’re finally getting fit but your finances are a mess.

We are going to break down exactly how to build a strong health foundation that actually gives you more energy for everything else, plus explore the real connection between life balance and money-because financial stress impacts every decision you make. You’ll also discover why your mental state acts as the control center for all of your choices, and learn a practical approach to strengthen all three areas without burning out.

Stop playing whack-a-mole with different parts of your life. Everything gets easier when these three pillars support each other.

Understanding the Interconnectedness of the Life Balance

How it is that when one pillar is neglected, a chain reaction takes place throughout each area.

Picture this: You are crushing it in the gym, meal prepping like a boss, but your bank account is bleeding money every month. The stress of not knowing how you’re going to make ends meet starts to eat at you. You begin to lose sleep, skip workouts to pick up extra shifts, and in a heartbeat, that healthy lifestyle you worked so hard to build crumbles. This is not an accident; this is the interlinked reality of life balance.

When one begins to weaken, there is no way the others wouldn’t give in. Financial stress triggers cortisol production, disrupting sleep patterns and weakening immune function. Poor health leads to medical bills and lost productivity, thus greater financial strain. Mental fatigue from either situation leads to clouded judgment and bad choices, which then exacerbate problems in all areas.

It’s a two-way domino effect: strong financial health reduces stress hormones, thereby improving physical recovery and mental acuity. Good physical health will give you more energy and enhanced brain power, potentially boosting your earning ability. A stable mental state allows for better financial decisions, healthier lifestyle choices.

The science of holistic wellness & peak performance.

Neuroscience research shows why life balance and money management, physical health, and mental wellness function as one integrated system. The prefrontal cortex-a part of the brain in charge of executive function and decision-making-gets compromised when one area is under chronic stress.

It has been documented that financial stressors activate the same neural pathways as physical pain, flooding the brain with stress hormones that impair memory, focus, and immune function. On the other hand, regular exercise increases the level of BDNF, which helps in enhancing cognitive function and emotional regulation thereby having a direct effect on one’s decision-making abilities in financial matters.

The vagus nerve connects brain and body exquisitely. Appropriate breathing, exercise, or other stress management, which stimulate it, all work to improve physical recovery and harden the mind while dampening inflammation, which predisposes a person to anxiety and bad decisions.

Why the traditional approaches to self-improvement fail

Most self-improvement strategies attack problems in isolation. You address debt while not really tackling the stress-eating that’s draining your budget. begin a fitness routine without fixing the sleep schedule that sabotages your workouts. You practice mindfulness while you ignore the financial anxiety that keeps your nervous system activated.

This siloed approach ignores how these systems communicate. The human body doesn’t compartmentalize stress-it responds to the total load. You fix one area and neglect others, creating unsustainable pressure that will eventually break the weakest link.

More conventionally, these approaches focus on willpower rather than systems. Willpower is depleted throughout the day and is unreliable under stress. In times of financial pressure or health-related issues, good intentions readily crumble without the right support structures in place.

ALSO READ : How to Make Money Without BurnOut Your Life

Breaking free of the single-focus improvement trap

Real change happens when you begin to view your life as an ecosystem, in which health and finances and mental state are literally affecting one another, constantly. The culture ignores this by framing this as an either-or choice: pay down debt OR join a gym. People who successfully change know these investments mutually reinforce one another.

Start by noticing where stress in one area is sabotaging another. Observe how money worries affect your sleep, or poor health affects your earning potential, or how mental fatigue leads to expensive convenience choices. These patterns show you where integrated solutions can create multiple wins.

Build habits that serve multiple pillars simultaneously. For example, cooking at home improves health AND finances while providing routine to combat stress. Walking meetings boost your fitness AND productivity while clearing the mental fog. Creating budget categories for health investments acknowledges their financial value.

The ideal is not balance; it is purposeful integration of elements, where the upper trajectory of one improvement curve reinforces other gains to drive upwards spirals, rather than destructive cycles.

Building Your Foundation of Health for Total Life Success

Creating sustainable energy levels to fuel your financial and mental performance.

Your body energy directly drives your every financial decision and mental battle. Your brain assimilates information at a faster rate when the body is working like a fine-tuned machine, your stress tolerance increases, and your ability to spot opportunities sharpens dramatically.

Think about your most productive days. You likely woke up refreshed, moved your body somehow, had nourishment, and your mind felt pretty sharp all day long. That is no accident: your physiology was priming your cognition to succeed.

Energy management trumps time management every day of the week. You can have all the hours in the world, but if you lack sustained energy, those hours are wasted potential. People who can sustain their energy throughout their day are the ones that make better investment decisions, negotiate more effectively, and avoid costly mistakes that are the result of being fatigued.

It’s all about treating your body as the high-octane machine that it is. You wouldn’t put cheap fuel in a Ferrari; similarly, you can’t expect peak performance mentally and with your finances when your base is lagging.

Define daily non-negotiables that have a compounding effect over time.

Small, consistent actions create huge results with time over months and years. The habits you create around your health directly affect your ability to build wealth and keep mental clarity.

Your morning routine sets the tone for everything that follows. Whether it’s 20 minutes of movement, a protein-rich breakfast, or five minutes of deep breathing, these deceptively small choices have ripples throughout your entire day.

Essential daily habits that maximize your potential:

Morning movement: Even 10 minutes gets your blood flowing and brain firing

Tracking hydration: Dehydration kills mental sharpness faster than anything

Protein at every meal: Stable blood sugar equals stable mood and decision-making

Digital boundaries: protect your attention span, protect your earning potential

Consistent sleep schedule: Your brain literally cleans itself during quality sleep.

But the real magic happens once these habits become automatic. You’re no longer using up valuable mental real estate deciding whether you should go to the gym today or what to eat for breakfast this morning. That saved mental bandwidth gets redirected toward more important decisions-like furthering your career or managing your investments.

Better sleep and nutrition for higher capabilities of decision making.

Sleep is not recovery time; it is the time your brain uses to process information, solidify memories, and get ready for peak performance. Those who consistently report 7-9 hours of quality sleep made better financial decisions and handled their stress better.

Poor sleep sets off a cascade of problems. Impulse control falters, making over-spending and emotional investing much more likely. Stress hormones shoot higher, acting in concert to not only sour your mood but dull your thinking of long-term goals.

Sleep optimization strategies include

Keep your bedroom cool, dark, and quiet

Avoid eating 3 hours before bedtime

Create a bedtime routine that tells your brain it’s time to be sleeping.

Limit blue light exposure after sunset

Get up at the same time every day, even on weekends

Nutrition directly affects the functioning of your brain. Since your brain requires about 20% of your daily intake of calories, the quality of fuel becomes very important. While processed foods give you energy spikes and crashes that knock you off productivity, whole foods provide steady, sustained mental energy.

Focus on foods that regulate blood sugar: lean proteins, healthy fats, complex carbohydrates, and plenty of vegetables. When the blood sugar remains balanced, your mood is balanced, your focus remains high, and your decision-making dramatically improves.

You know immediately from the definition that there’s a very strong connection between life balance and money, because your physical impacts your earning potential and your ability to make good financial decisions.

Master financial wellness to become your security pillar.

Developing money mindsets that reduce stress and anxiety

Money stress doesn’t stop at impacting your bank balance; every aspect of your life is affected, it disrupts sleep, strains relationships, and lets down health. And the key to stopping this all lies within reshaping what you think about money itself.

You start by acknowledging one thing: money is a tool, not a benchmark of your worth. The moment you link your self-worth to your net worth, every financial setback becomes a personal failure. Instead, bring yourself to think of money as energy that goes in and out of your life quite naturally. This shift alone can dramatically reduce the emotional weight you carry around finances.

Practice abundance thinking by focusing on opportunities, not limitations. This means that instead of saying, “I can’t afford that,” reframe your way of thinking with the question, “How can I create the income to afford that?” This simple reframe opens your mind to solutions rather than reinforcing scarcity beliefs.

Keep your identity separate from your financial situation. You are not your debt, your salary, or your investment portfolio. These are temporary circumstances that can change with the right strategies and time.

I help create automated systems that free up mental bandwidth.

Your brain is only capable of so many decisions, and constant money management siphons off that precious resource. Automation frees up your brain from mundane financial chores and helps establish routine in your financial life.

Set up automatic transfers to your savings account the day after payday. When the money moves before you see it, you will not miss it. This “pay yourself first” approach eliminates the temptation to spend what should go into savings.

Automate bill payments to avoid late fees and the mental stress of tracking due dates. Use calendar reminders for the irregular expenses, such as premiums for insurance or annual subscriptions.

Set up automatic investment contributions to your retirement accounts and investment portfolios. Automating investments uses dollar-cost averaging to take the rollercoaster out of market volatility and builds consistent wealth.

Utilize banking apps designed to round up purchases and save spare change. These micro-savings add up, without much effort or any sacrifice, whatsoever.

Building emergency funds to protect your health and peace of mind

Your emergency fund acts like a buffer-a money shield, or even your financial immune system-against the surefire curveballs life throws your way. Without such a buffer, unexpected expenses will perhaps whisk you away into debt cycles that generate chronic stress, which is a clear and present danger to your body and mind.

Start with the goal of $1,000 and build to three to six months of living expenses. This may sound overwhelming, but remember that any dollar amount is one step closer to a financially secure position. Even $100 in savings will keep you from overdrafting on your account or using a credit card for a minor emergency.

Keep your emergency fund in a separate, easily accessible savings account. The separation prevents accidentally spending it, and the accessibility ensures you can handle true emergencies without delay.

Consider how financial security links to health. If you know you can cover unexpected medical bills or car repairs, your stress level will drop dramatically. This minimized level of stress will strengthen your immune system, improve your sleep quality, and enhance your overall well-being.

Aligning spending with values and long-term goals

True life balance arises when your spending accurately reflects what is most important to you. Mindless consumption causes disconnection between your money and your values; the result can be buyer’s remorse and financial regret.

First, identify your core values and life goals. Do you value experiences over possessions? Is it more important to spend time with the family than to advance your career? Are you passionate about traveling, educational endeavors, or giving something back to the community? These should be your priorities when making decisions about spending.

Create a values-based budget that allocates money to what brings you joy and fulfillment. Slash ruthlessly in categories that don’t align with your priorities; spend generously on what does.

Track what you spend, but not with judgment, for a month. Then go back and categorize each of those expenses into either serving or not serving these goals. You’ll often be surprised by the patterns that emerge and the opportunities to realign.

Practice intentional spending: institute a 24-hour rule for non-essential purchases above some amount. The pause helps you to think whether the purchase serves your long-term vision or is just an impulsive decision by emotional or social pressure.

Remember, what is life balance if not the harmony of your resources with your authentic desires? As your money flows toward your genuine priorities, financial stress will start to decrease on its own, making room for the other pillars of balanced living to come through.

Strengthening Your Mind as Your Control Center

Developing emotional resilience, which makes one better equipped to handle financial setbacks.

Your mind is the command centre for everything else in your life. When financial storms arise, your emotional resilience will be the determinant on whether you get up stronger or spiral into other worse problems. Creating such strength starts with reframing one’s view about money challenges.

Instead of seeing a job loss or unexpected expense as a personal failure, resilient people treat these events as temporary obstacles that require problem-solving. This mental shift protects you from the shame and panic that often lead to poor financial decisions. Practice separating your self-worth from your bank account balance. Your value as a person doesn’t fluctuate with market conditions or monthly income.

Establish a “setback recovery protocol” before you actually need one. Write down three concrete steps you will take when financial stress strikes: whom you will call for support, which expenses you will cut first, and how you will generate additional income. Having this plan removes the emotional guesswork during those crisis moments.

Building stress management techniques that protect physical health

The chronic stress of money worries acts like a poison on the body, creating a downward spiral in which health declines and medical costs rise, while earning capacity is reduced. To break such a cycle demands active management of stress to make it as much a part of daily routine as brushing your teeth.

Deep breathing exercises work wonders for financial anxiety. The next time you catch yourself racing from bills or debt, try the 4-7-8 technique: inhale to the count of 4, hold for 7, exhale to the count of 8. This turns on your parasympathetic nervous system and halts the cascade of stress hormones eroding your immune system.

Physical activity also helps on another front: it reduces stress hormones and, at the same time, builds up your energy to tackle your financial goals. You don’t need any expensive gym memberships. The 20-minute walk while listening to a financial podcast combines stress relief with education. Regular exercise will also help you sleep better, which directly impacts your decision-making abilities the next day.

Mindfulness practices that could enhance financial decision-making

Mindfulness changes your relationship with money by inserting space between impulse and action. Most financial mistakes are done at times when feelings drive decisions instead of logic. Mindful awareness helps you catch those moments before they cost you money.

When you think about making a purchase for over $50, stop and take three conscious breaths. Ask yourself, “Is this something I’m purchasing because I need it, or am I feeling something right now?” Shopping often gets used as a mode of regulating emotions rather than taking care of needs. For so many people, this simple pause saves more money than complex budgeting systems.

Practice mindful money monitoring: check the balance in your accounts without judgment. Most of us don’t look at our finances on a day-to-day basis because we feel shamed or frightened about what we’ll discover. Mindfulness helps you learn to contemplate financial reality with interest, not judgment. This neutrality of emotions makes patterns more easily identifiable and quicker adjustments possible.

Creating mental frameworks that will sustain motivation in all areas of life.

The sustainable balance of life requires mental models that will connect day-to-day actions with a bigger vision. Without these frameworks, when immediate results do not appear, motivation fades. You want to construct systems reinforcing positive behaviors in the domains of health, finances, and mental wellbeing at the same time.

Create a “compound effect mindset” in which small, consistent actions in one area support progress in others. Examples include packing healthy lunches, which saves money as much as it improves nutrition and reduces stress from daily food decisions. Walking to nearby errands combines exercise with transportation savings. It is in these crossover benefits that sustainable change is created.

Track the leading measures, not the lagging measures. Without obsessing over your weight, bank balance, or stress level, for example, the leading measures would be the number of steps taken, money saved, or meditation minutes logged that day. These process metrics immediately feed back information and keep motivation at an all-time high during slower progress.

Build into your schedule weekly “life balance reviews” where you review progress across all three pillars. This prevents tunnel vision, where success in one area masks problems that are developing in another. True life balance and money management tie together when your mental frameworks support integrated thinking, rather than compartmentalized goal-setting.

Applying the Integrated Approach for Lasting Results

Design daily routines that target all three pillars at once.

The key to true life balance is in designing daily routines where health, finances, and mental well-being blend in as opposed to added tasks. Your morning routine is where it all begins-get your mental state aligned with five minutes of mindful breathing, plan your day with a review of your financial goals over coffee, and add some movement to energize your body. This integrated approach saves time and reinforces the connections between all three areas.

Consider batch-processing activities serving many pillars. Sunday meal-prep sessions empower your health via nutrition planning, support your financial goals via the avoidance of impulse buys of food, and clear your mind via organized preparation. Walking meetings marry physical activity with productivity at work; podcasts about personal finance played during workouts feed your mind and body at the same time.

Evening routines, too, need to reflect this integration: reflect on the wins of your day in all three areas, plan tomorrow’s priorities while you’re stretching, and do gratitude that acknowledges the progress made in health, wealth, and mental peace. It makes this-what is life balance-a concrete daily action instead of an abstract question.

Building systems of accountability that reinforce the dimensions of balanced progress

Building accountability is about going further than simple self-monitoring to systems that organically guarantee progress in all three pillars. Find yourself a partner in crime who has similar goals, which means not just finding a workout buddy or a financial advisor but someone committed to holistic growth. Set up weekly check-ins that also include your physical energy, financial milestones reached, and mental clarity.

Digital tools can really amplify accountability. Use apps that track multiple life areas all at once; conversely, avoid the trap of over-monitoring. Pick three key metrics-one from each pillar-and focus on consistency, not perfection. Let your progress be public through social media or a blog, and through doing so, allow that external pressure to motivate continued effort.

Professional accountability works powerfully when well integrated. The therapist may help you understand how financial stressors impact your mental health, while the financial advisor should know about health expenses that impact your budget. The doctor needs to understand work stress that affects physical symptoms. This is how all of your support systems can work in concert rather than in isolation from one another.

Tracking metrics that expose the interrelationships within your three pillars

Effective tracking is more than counting steps taken, dollars saved, or minutes spent in meditation. Find those leading indicators showing how the improvement of one area positively influences another area. Track your energy levels simultaneously with your bank account balance because you may find out that financial stress directly matches your fatigue and poor choices of food.

Create a simple weekly scorecard that captures the interconnections. On a scale of 1 to 10, score your physical energy, financial confidence, and mental clarity. Note the patterns. You often can find that high-stress weeks coincide with overspending and poor sleep, or that consistent exercise improves both your mood and the ability to make smart financial decisions.

Follow lifestyle metrics across multiple pillars. How often do you cook at home versus ordering takeout? This single metric reveals your financial discipline, nutritional choices, and stress management all in one. Now monitor your sleep quality against your productivity and spending patterns: poor rest often leads to both decreased earning potential and increased impulse purchases.

The key will be to find the minimum effective dose of tracking that conveys insight without becoming overwhelming. Select metrics that naturally encourage the behaviors you want to reinforce, across all three areas.

Adjusting course when life requires you to shift your focus.

Life balance and money management are both about flexibility when life throws up inevitable challenges. Job loss might mean you have to prioritize financial stability temporarily, but that does not necessarily mean you should stop being healthy and mentally well. Adapt your approach-replace expensive gym memberships with free bodyweight workouts, swap expensive therapy sessions for peer support groups, and find low-cost ways to manage stress.

In times of health crises, financial and mental strategies alike must adjust to accommodate recovery. This could be budget adjustments for medical expenses without compromising the emergency fund or adjusting work to minimize stress without sacrificing long-term financial security. The aim is not to lose momentum in anything, even if the pace of activity changes. Career changes, family shifts, or significant life moments will inevitably blow up your routines.

Successful adaptation means rapidly determining which pillar needs urgent attention while you’re keeping the other areas to minimum viable habits. Keep a “crisis mode” plan that tells you what your most critical non-negotiables are—maybe ten minutes of movement, check your bank balance, and one deep breathing exercise daily. Remember, temporary imbalances are normal and required. The integrated approach isn’t about perfect balance every day; it is about making sure your three pillars support each other through whatever life throws your way. Regular reassessment and gentle course corrections keep you moving toward your long-term vision of balanced success.

Life balance is a function of not just juggling three different realms but achieving unity among your health, finances, and state of mind. When you build up one leg of your pillow, the other two will benefit.

A good physical health will provide you with all the energy you need to accomplish your financial objectives, and financial security will reduce your worries and promotes improved mental clarity. Your mental state serves as a control room, which assists you in making wise decisions concerning both your body and your money. The key is to make small steps in all three categories rather than trying to focus on one area.

Begin with isolating which pillar you need to focus on at the moment and construct basic habits to bridge to the other two. Remember that challenges in one realm need not upend your whole life – the power of your other pillars will help you during hard times. Start with one step today towards all three pillars, and watch how this integrated approach will change not only your daily life but your entire whole quality of life.

Written by Azhar Huzaifa

Azhar Huzaifa is the founder of LifeBalanceInsight.com.

He writes about money psychology, health, and life balance,

helping middle-class families reduce stress and live better lives.

1 thought on “The Three Pillars of Life Balance: Why Your Health, Finances, and Mental State Must Work as One”